Nick Goetze discusses fixed income market conditions and offers insight for bond investors.

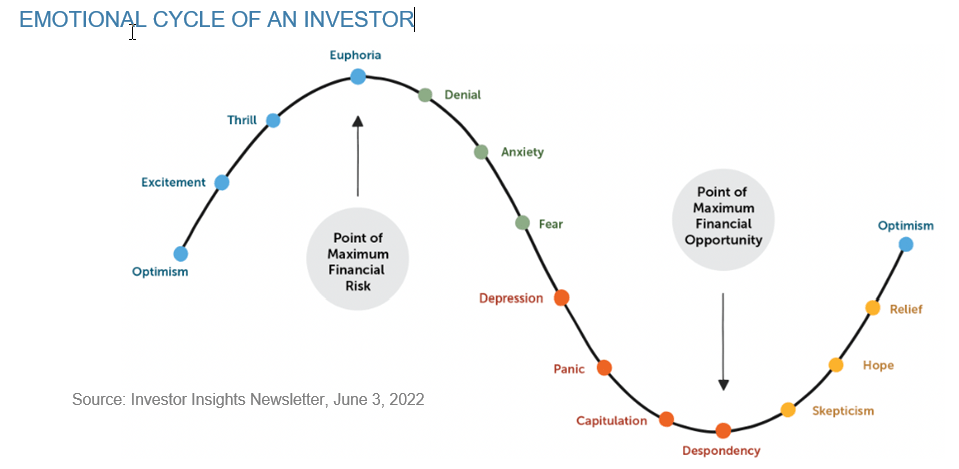

Recency bias is the tendency to give more weight to recent events than past events, which can lead to skewed judgments. It can make us more confident when things are going well and more pessimistic when things are not. This can influence our decisions as we often assume the current trend will continue. On the investment front, recent markets have given most of us a lot of confidence. After all, we have seen higher rates on bonds and extended double digit returns in the S&P 500 index. The further we get from the last time things were not so easy, the more confident we get. The chart below shows the typical emotional cycle of an investor.

While there is no way to know exactly where we are on the cycle it is likely in the vicinity of euphoria. Typical investor behavior in this part of the cycle involves taking on more risk as recency bias makes us comfortable with the potential for greater volatility. What follows is often the problem. By the time we get to the panic phase, rational decision-making becomes more difficult. We ideally buy stocks when equity markets are depressed and sell bonds when yields are low, yet the opposite often plays out. At times of stress, people capitulate by selling stocks and buying bonds. In other words, selling stocks at the low and then buying bonds at the high. This is especially dangerous for investors in retirement who are depending on portfolio income to support their lifestyle.

Now is the time to prepare for the next negative cycle in our economy. We do not know when this will occur, but it always does as a normal part of an economic cycle. In the fixed income space, there are two ways to prepare. First; you can build a custom portfolio of individual bonds that can produce enough income to support your normal lifestyle. Once that is in place, you may not panic at the bottom of the emotional cycle because you are not concerned with how to create the cash flow you need. Second; you can buy short-term bonds in the amount you will need to live your lifestyle, going out two to three years. Each year you can add another three-year investment. This will give an investor the comfort of knowing they have time to carefully plan how to address a downturn if one should occur. The next three years of cash flow are taken care of, allowing for time to contemplate during a downturn. In both cases you can then invest the remainder of your portfolio in risk-based assets because you can ride out the proverbial storm.

The general rule of thumb in retirement is to plan on a 4%, draw on assets. Currently, investment grade taxable bonds can yield between 4% to 5% and even higher in some cases, for IRAs, charitable endowments, lower tax bracket investors and pensions. Tax free municipal bonds on the longer half of the curve are yielding more than 4%. It was not that long ago that most yields were less than half of what they are now. Especially for retirees, it is time to look at creating stable cash flow with known outcomes in individual bonds. Without the concern of how to support your lifestyle, hopefully in the next downturn you will be adding confidently to riskier investments at the bottom instead of letting panic drive decisions. Once a custom bond strategy is implemented, it will perform regardless of what interest rates do going forward. At Raymond James, our fixed income department takes great pride in supporting our financial advisors in pursuit of using individual custom bond portfolios to help create the cornerstone of retirement success.

The author of this material is a Trader in the Fixed Income Department of Raymond James & Associates (RJA), and is not an Analyst. Any opinions expressed may differ from opinions expressed by other departments of RJA, including our Equity Research Department, and are subject to change without notice. The data and information contained herein was obtained from sources considered to be reliable, but RJA does not guarantee its accuracy and/or completeness. Neither the information nor any opinions expressed constitute a solicitation for the purchase or sale of any security referred to herein. This material may include analysis of sectors, securities and/or derivatives that RJA may have positions, long or short, held proprietarily. RJA or its affiliates may execute transactions which may not be consistent with the report’s conclusions. RJA may also have performed investment banking services for the issuers of such securities. Investors should discuss the risks inherent in bonds with their Raymond James Financial Advisor. Risks include, but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and duration. Past performance is no assurance of future results.

Investment products are: not deposits, not FDIC/NCUA insured, not insured by any government agency, not bank guaranteed, subject to risk and may lose value.

To learn more about the risks and rewards of investing in fixed income, access the Financial Industry Regulatory Authority’s website at finra.org/investors/learn-to-invest/types-investments/bonds and the Municipal Securities Rulemaking Board’s (MSRB) Electronic Municipal Market Access System (EMMA) at emma.msrb.org.