Raymond James Chief Economist Eugenio J. Alemán discusses current economic conditions.

Yes, this time is different, but not because inflation itself is unprecedented. What has fundamentally changed is the macroeconomic starting point. Unlike the post-Global Financial Crisis period, when persistent disinflation and repeated downside surprises dominated policy decisions, the economy today is operating in a world where structural disinflation is no longer the default backdrop. That shift has important implications for monetary policy and, ultimately, for markets.

In the decade leading up to the pandemic, the Federal Reserve (Fed) adopted a deliberately patient approach to inflation, allowing price pressures to overshoot the target for extended periods before responding. That framework was a rational response to nearly twenty years of disinflationary forces ranging from globalization to technological change that continually pushed inflation below target. However, that same framework proved ill-suited for the post-pandemic recovery. With hindsight, the Fed should have begun tightening policy earlier as inflation emerged in 2021. But even if the Fed had increased rates immediately as it should have, it is highly unlikely that they would have been able to prevent the increase in inflation and contain Americans as they rushed to “living la vida loca” after years of sheltering in place and postponed consumption. In that environment, it is difficult to imagine an interest-rate level capable of meaningfully restraining spending without causing severe collateral damage to growth and employment. Policy was behind the curve, but the curve itself was unusually steep.

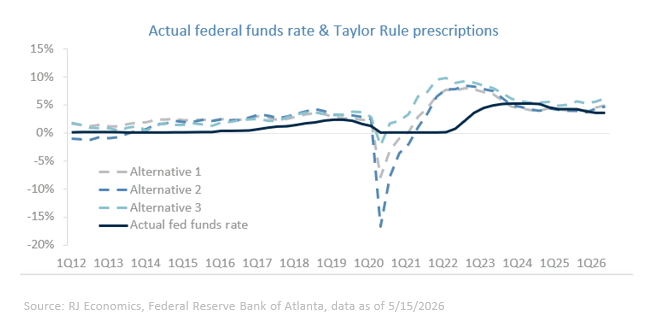

Standard policy benchmarks reinforce this point. Taylor Rule estimates suggest that monetary policy during the recovery was materially more accommodative than warranted, with implied policy rates at times approaching double digits (see graph below). Even under more conservative assumptions, prescribed rates were well above the levels actually in place, underscoring how far policy lagged shifting inflation dynamics. By the time liftoff finally began in early 2022, inflation had already surged close to 8% year over year, forcing the Fed into a far sharper tightening cycle than markets had anticipated.

Fast forward to today, and the policy landscape looks very different. The Fed is no longer constrained by the zero lower bound, and global disinflation can no longer be taken for granted. While fiscal expansion remains an upside risk to prices, the more immediate concern is that inflation has lost its pre-pandemic anchoring. Even setting aside tariffs and recent oil price increases tied to geopolitical tensions with Iran, inflation is no longer gravitating back toward the stable sub-2% environment that characterized the prior cycle. That reality sharply reduces the Fed’s room for patience.

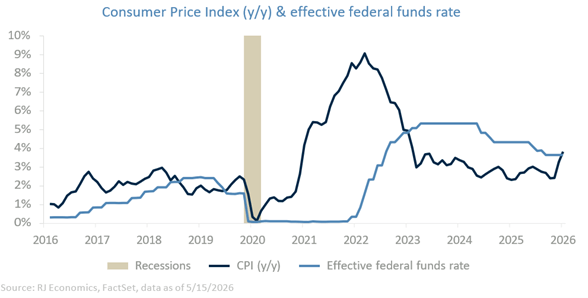

Recent CPI, PPI, ISM price indices, and import price reports underscore this point. While April’s CPI included some one-off distortions – most notably in shelter costs linked to last year’s government shutdown – broader price pressures were evident across multiple categories. The PPI data are even more concerning, suggesting pipeline pressures that could bleed into consumer prices over the coming quarters. ISM prices indices, which are important forward-looking indicators, reached three-year highs in April, showing that input prices are affecting both manufacturing and service industries. Lastly, import prices experienced their largest monthly increase since March 2022, the period immediately following the onset of the Russia–Ukraine conflict. These reports do not demand an immediate rate hike, but they materially raise the odds that the policy discussion shifts from when cuts begin to whether further tightening may be required.

From a market perspective, this matters less for the next meeting and more for the trajectory of expectations. The longer inflation remains above target, the harder it becomes for the Fed to credibly signal an easing cycle, particularly in an environment characterized by expansionary fiscal policy, resilient growth, a gradual recovery in labor markets and sustained capital investment tied to artificial intelligence. Add continued energy price risks to that mix, and the bias of policy risk tilts meaningfully in one direction.

Bottom line

The rate conversation is set to intensify over the coming months. Markets are once again being forced to confront a world in which policy rates may stay higher for longer – or even move higher – rather than glide lower as soon as growth moderates. The arrival of a new Fed chair this month adds another layer of uncertainty, as shifts in leadership can influence both communication and policy direction. Taken together, the policy outlook is becoming more uncertain with fewer clear signals on the path forward.

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those of Raymond James and are subject to change without notice. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur. Past performance may not be indicative of future results.